March 13, 2026

The Hidden Cost of Rising Home Values

Rising home values are generally welcomed by homeowners they signal stronger equity, a healthier neighborhood, and a more valuable asset. But there is a financial consequence that tends to arrive quietly, often months or years later: a noticeably higher property tax bill. According to CoreLogic (January 2026), U.S. property tax payments climbed 27.4% between 2019 and 2025 outpacing wage growth for the majority of American households and catching many owners off guard.

This article breaks down exactly how the relationship between home prices and property taxes works, which states are feeling it most, and critically what steps homeowners can take right now to ensure they are not overpaying. You can also explore our related guides on the TaxCutter.us.

How Home Values Drive Property Taxes

Property taxes operate on a principle known as ad valoremLatin for according to value. In practice, this means that your annual tax liability is calculated by multiplying your home’s assessed value by your local tax rate. When assessed values rise, as they have consistently across the U.S. since 2020, tax bills follow automaticallyregardless of whether you have made any changes to your property or your finances. In such cases, homeowners often turn to property tax reduction strategies to ensure they are not overpaid.

The mechanism is straightforward, but its impact compounds quickly. Even a modest 20% appreciation in value entirely normal in many markets over the past three years translates to a substantial jump in your annual bill.

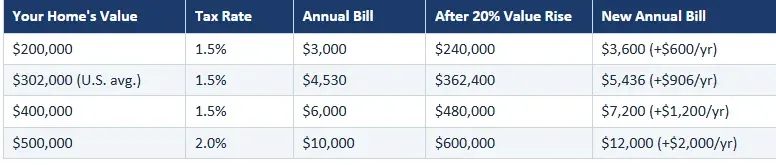

How Much Have Values and Tax Bills Actually Risen?

The scale of recent increases is difficult to overstate. The housing boom of 2020 to 2023 compressed years of normal appreciation into just a few years, and local appraisal districts have been steadily reassessing values to reflect those gains ever since. In the states where prices rose most aggressively, the corresponding tax increases have been equally dramatic. Based on CoreLogic data from January 2026:

At the national level, the median U.S. property tax bill reached approximately $3,018 in 2025 and is projected to approach $3,500 by end of 2026 a 4.2% year-over-year increase that shows little sign of easing in the markets most affected by the earlier price surge.

The Lag Effect: Why Tax Bills Keep Rising

One of the more counterintuitive aspects of property taxation is the reassessment of lag. Unlike financial markets, which respond to changes almost instantly, local appraisal districts typically operate on a fixed reassessment cycle often running one to three years behind actual market conditions. This creates a situation where homeowners in a market that has since cooled are still receiving inflated tax bills based on valuations from the peak of the boom, making a property tax protest an important step for those seeking accurate assessments.

Many homeowners are still absorbing the full financial weight of the 2021–2022 price surge, with local governments processing those peak-year reassessments only now. For anyone who assumed their tax liability had stabilized alongside the market, a spring 2026 appraisal notice may come as an unpleasant surprise one that may require a Texas tax protest to correct.

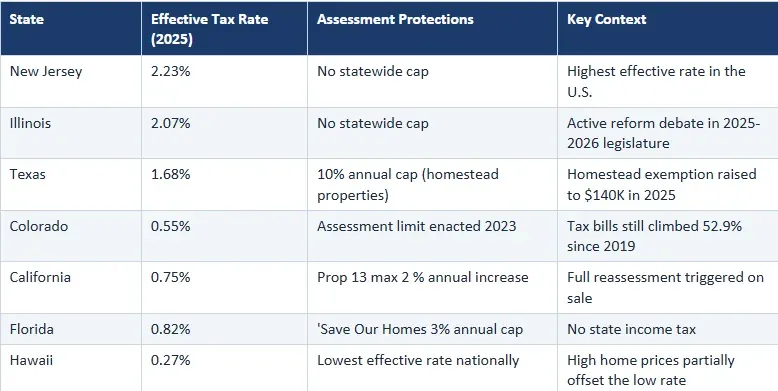

States Most Exposed to Rising Property Taxes

Exposure to rising property tax bills varies considerably by state. Some jurisdictions have enacted assessment caps statutory limits on how much an appraised value can increase in any given year, regardless of market conditions. As of 2026, 18 states and Washington D.C. have these protections. Many others leave homeowners fully exposed to market-driven reassessments.

The Wider Impact of Rising Property Taxes

The consequences of sustained property tax increases extend well beyond an individual homeowner’s budget. Across the housing market, rising tax burdens are reshaping affordability, mobility, and financial stability in ways that deserve careful attention making a property tax protest an increasingly important step for many homeowners. Monthly mortgage payments increase as escrow adjustments automatically raise payments, even without changes in interest rates. At the same time, purchasing power for buyers erodes, as lenders factor higher property taxes into debt-to-income ratios, often reducing what buyers can afford in high-tax markets.

Delinquency rates are also climbing, with recent research showing an increase in mortgage stress in regions where property taxes and insurance costs are rising the fastest. Seniors and fixed-income homeowners are particularly affected, as they lack the income flexibility to absorb rising tax burdens. Additionally, assessment caps in some states create a “lock-in” effect, discouraging homeowners from moving due to the loss of tax protections. In contrast, in states like Texas, a Texas tax protest can serve as a practical way to address rising assessments and maintain financial stability.

Practical Steps Every Homeowner Should Take

While broader market forces are largely outside any individual’s control, there are meaningful steps homeowners can take to ensure they are not paying more than their fair share. Four actions stand out as particularly effective:

1.Verify That Every Available Exemption Has Been Filed

Rising Most states provide a homestead exemption that directly reduces the taxable value of a primary residence but it must be applied for. Texas recently raised its homestead exemption to $140,000, yet many eligible homeowners have not submitted the application. Additional exemptions for seniors, veterans, and qualifying disabilities are widely available and frequently go unclaimed. Texas residents can apply via the Texas Comptroller’s Exemptions page.

2.Review Your Annual Notice of Appraised Value

Each spring, your County Appraisal District issues a Notice of Appraised Value the figure upon which your entire tax bill is based. This notice deserves careful scrutiny. Cross-reference the assessed value against recent comparable sales in your immediate area. If the figure is materially higher than what your property would realistically command on the open market today, you have a substantive basis for a formal challenge.

3. File a Property Tax Protest If the Assessment Appears Excessive

Contesting your appraisal is free of charge, procedurally straightforward, and critically carries no risk of increasing your bill. In Texas, the filing deadline falls on May 15 each year, or 30 days from the date your notice was issued, whichever comes later. visit TaxCutter.us.

4 .Stay Informed About State and Local Relief Programs

Significant relief is already in motion across the country. Texas has committed $51 billion to property tax relief in 2025-2026. New Jersey’s Stay NJ program begins distributing quarterly payments to qualifying homeowners in 2026. Multiple other states are actively legislating new assessment caps and expanded exemptions. The Tax Foundation’s state-by-state property tax tracker is an authoritative resource for monitoring developments in your state.

What Homeowners Can Do to Reduce Property Taxes

The relationship between rising home prices and escalating property tax bills is well established, and the lag inherent in the reassessment process means many homeowners are still contending with the full consequences of the 2020–2023 housing surge. But this is not a situation in which homeowners are without recourse. Claiming every eligible exemption, reviewing assessments annually, and filing a property tax protest when valuations appear excessive are straightforward actions that can meaningfully reduce a tax liability year after year. visit TaxCutter.us.